SEBI has proposed certain amendments to the SEBI (Substantial Acquisition of Shares and Takeover) Regulations, 1997 ("Takeover Code") and has invited public comments before January 24, 2004. Some of the major proposals relate to:

The definition of 'promoter' has been substantially revised to include any person or persons who are in direct or indirect control of the company or any persons who are named as promoters in the offer document or in the shareholding pattern disclosed under the provisions of the Listing Agreement ("LA"), whichever is later.

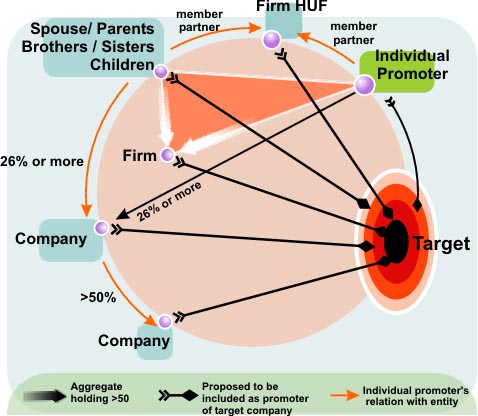

In case the promoter is an individual, the persons who shall be deemed to be promoters as per the proposed amendment, is represented by Figure 1 (Fig.1).

FIG. 1

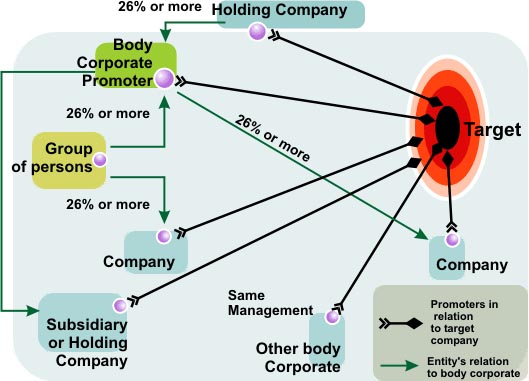

In case the promoter is a body corporate, entities that shall be deemed to be promoters as per the proposed amendment is represented by Figure 2.

FIG. 2

It is proposed that Financial Institutions, Scheduled Commercial Banks, Foreign Institutional Investors and Mutual Funds shall not be deemed promoters merely by reason of their shareholding; they shall however, be deemed promoters of their subsidiaries and the mutual funds that they sponsor.

The regulation granting exemption to the inter-se transfer of shares amongst the promoters from applicability of the Takeover Code is sought to be amended by defining the term "promoter" under this clause. This inclusion is intended to keep the exemptions under this clause to a minimum.

The term 'public shareholding' is sought to be defined as the shareholding by persons other than the promoters.

As per the current regulations, an acquirer (together with the persons acting in concert with him) holding 15% or more but less than 75% of the paid-up capital of a company can consolidate his holdings upto 5% of the paid-up capital in any financial year under the creeping acquisition route, without having to make an open offer. Under the proposed amendment, it has been proposed to reduce this threshold limit for exemption under the creeping acquisition route to 51% from the current 75%.

An open offer to be made under the Takeover Code has to be for a minimum of 20% of the voting capital of the company. It is proposed to qualify this requirement by providing that the acquisition under a public offer must not result in the public shareholding in the company being reduced to a level below the minimum specified in the LA for purposes of continued listing.

It is also proposed that in the event that the open offer under the Takeover Code is triggered due to the acquisition of control over the target company, and consequent to such open offer, the public shareholding falls below the limit specified in the LA for purposes of continued listing, the acquirer shall have the option to buy the outstanding shares in accordance with the Delisting Guidelines. Alternatively, the acquirer can undertake to raise the level of public shareholding to the levels specified for continued listing under the LA by a fresh issue of shares or disinvestment of his holding through an offer for sale or sale in the secondary market in a transparent manner. These options have to be exercised within a period of six months from the date of closure of the public offer.

Disclaimer

The contents of this hotline should not be construed as legal opinion. View detailed disclaimer.

SEBI has proposed certain amendments to the SEBI (Substantial Acquisition of Shares and Takeover) Regulations, 1997 ("Takeover Code") and has invited public comments before January 24, 2004. Some of the major proposals relate to:

The definition of 'promoter' has been substantially revised to include any person or persons who are in direct or indirect control of the company or any persons who are named as promoters in the offer document or in the shareholding pattern disclosed under the provisions of the Listing Agreement ("LA"), whichever is later.

In case the promoter is an individual, the persons who shall be deemed to be promoters as per the proposed amendment, is represented by Figure 1 (Fig.1).

FIG. 1

In case the promoter is a body corporate, entities that shall be deemed to be promoters as per the proposed amendment is represented by Figure 2.

FIG. 2

It is proposed that Financial Institutions, Scheduled Commercial Banks, Foreign Institutional Investors and Mutual Funds shall not be deemed promoters merely by reason of their shareholding; they shall however, be deemed promoters of their subsidiaries and the mutual funds that they sponsor.

The regulation granting exemption to the inter-se transfer of shares amongst the promoters from applicability of the Takeover Code is sought to be amended by defining the term "promoter" under this clause. This inclusion is intended to keep the exemptions under this clause to a minimum.

The term 'public shareholding' is sought to be defined as the shareholding by persons other than the promoters.

As per the current regulations, an acquirer (together with the persons acting in concert with him) holding 15% or more but less than 75% of the paid-up capital of a company can consolidate his holdings upto 5% of the paid-up capital in any financial year under the creeping acquisition route, without having to make an open offer. Under the proposed amendment, it has been proposed to reduce this threshold limit for exemption under the creeping acquisition route to 51% from the current 75%.

An open offer to be made under the Takeover Code has to be for a minimum of 20% of the voting capital of the company. It is proposed to qualify this requirement by providing that the acquisition under a public offer must not result in the public shareholding in the company being reduced to a level below the minimum specified in the LA for purposes of continued listing.

It is also proposed that in the event that the open offer under the Takeover Code is triggered due to the acquisition of control over the target company, and consequent to such open offer, the public shareholding falls below the limit specified in the LA for purposes of continued listing, the acquirer shall have the option to buy the outstanding shares in accordance with the Delisting Guidelines. Alternatively, the acquirer can undertake to raise the level of public shareholding to the levels specified for continued listing under the LA by a fresh issue of shares or disinvestment of his holding through an offer for sale or sale in the secondary market in a transparent manner. These options have to be exercised within a period of six months from the date of closure of the public offer.

Disclaimer

The contents of this hotline should not be construed as legal opinion. View detailed disclaimer.