Corpsec HotlineSeptember 10, 2012 Indian Depository Receipt: Limited two-way fungibility allowedINTRODUCTIONThe Reserve Bank of India (RBI), the Indian central bank and the Securities and Exchange Board of India (SEBI), the Indian securities market regulator, have vide their respective circulars1 each dated August 28, 2012, paved the way for limited two-way fungibility for Indian depository receipt (IDR). Fungibility in this context refers to the ability of the holder of an IDR to convert such IDR into the underlying equity security and vice versa. Until now, the erstwhile regulations did not allow holders of underlying equity shares to convert such equity share into an IDR. However, redemption of an IDR into underlying equity shares was permissible subject to fulfilling certain conditions, such as, a minimum holding period of one year from the date of issue of IDRs and such IDR qualifying as an infrequently traded security on the stock exchange(s) in India. This regulatory position has now being modified by SEBI and RBI to provide for limited two-way fungibility for IDRs, similar to the fungibility available in case of an american depository receipt (ADR) or global depository receipt (GDR). BACKGROUNDAn IDR is basically a security listed on an Indian stock exchange, with its underlying being a listed security of a foreign incorporated and listed entity. The introduction of an IDR in the Indian securities market and the legal framework governing them was put in place with an objective to facilitate capital raising by foreign investors from domestic market, at the same time providing domestic investors an opportunity to make investments in securities of well-recognised multinational companies listed on developed markets. Till date, there is only one foreign company namely Standard Chartered Bank, Plc whose IDRs have been listed on an Indian stock exchange. The regulatory position with respect to IDRs has been evolving ever since the regulatory framework governing IDR was introduced by the Ministry of Corporate Affairs (MCA) in the year 2004. The following figure traces the series of regulatory changes with respect to redemption of IDR:

Figure 1: Evolution of regulatory framework governing fungibility of IDR The erstwhile Indian regulatory framework allowed only redemption / conversion of IDR into the underlying foreign security after fulfilling the prescribed conditions. The regulatory change would now enable even conversion of equity shares of a foreign issuer into IDR, to the extent of IDRs that have been redeemed / converted into underlying shares and sold. KEY CHANGES INTRODUCEDThe regulatory development allowing limited two-way fungibility flows from the announcement made by the then finance minister in his budget speech earlier this year. The following are some of the key highlights of this regulatory development:

TAX IMPLICATIONSPresently, there are no specific tax provisions under the Income-tax Act, 1961 with respect to tax implications at the time of redemption of IDRs into underlying equity shares. While SEBI and RBI have provided for limited two way fungibility, there exists no provision providing incentives under the tax laws to make the IDR regime attractive, viz, (i) any gains arising on redemptions of IDR into the underlying equity shares if not specifically exempt would lead to a situation of the holder being subjected to tax in the absence of any realised gains and hence making a redemption unattractive (ii) dividends received would be subject to tax as income from other sources and taxed at the regular tax rates applicable to the tax payer. CONCLUSIONThe rise of global finance has removed geographic boundaries for companies enabling them to raise capital in markets across the world. Issuance of depository receipts is an innovative mechanism especially for companies who are targeting to raise capital from a market other than the market of their primary listing. Depository receipts provide mutual benefits to issuers, investors as well as to the host market. Companies get to raise capital from willing investors, diversify their investor base and fulfill strategic objective such as for e.g. brand recognition. Investors get to invest in companies in which they otherwise could not have easily invested, diversifying their portfolio in the process. Ultimately, markets tend to become more efficient as increased access for investors through multiple listings enhances liquidity, and improves price-discovery. The regulatory change brought about to allow limited two-way fungibility is a step in the right direction, and it should make IDRs relatively more marketable. However, the results are more likely to be visible only when the other challenges faced by the Indian capital market are addressed.

1 Reserve Bank of India A. P. (DIR Series) Circular No. 19 (August 28 2012) and SEBI Circular No. CIR/CFD/DIL/10/2012 (August 28, 2012). 2 Reserve Bank of India A. P. (DIR Series) Circular No. 19 (July 22, 2009). 3 Reserve Bank of India A. P. (DIR Series) Circular No. 19 (August 28 2012) (para 2(i)). 4 The SEBI Circular (Circular No. CIR/CFD/DIL/3/2011 dated June 3, 2011) explains ‘infrequently traded’ to mean that the annualized trading turnover in IDRs during the six calendar months immediately preceding the month of redemption is less than five percent of the listed IDRs. DisclaimerThe contents of this hotline should not be construed as legal opinion. View detailed disclaimer. |

|

INTRODUCTION

The Reserve Bank of India (RBI), the Indian central bank and the Securities and Exchange Board of India (SEBI), the Indian securities market regulator, have vide their respective circulars1 each dated August 28, 2012, paved the way for limited two-way fungibility for Indian depository receipt (IDR). Fungibility in this context refers to the ability of the holder of an IDR to convert such IDR into the underlying equity security and vice versa.

Until now, the erstwhile regulations did not allow holders of underlying equity shares to convert such equity share into an IDR. However, redemption of an IDR into underlying equity shares was permissible subject to fulfilling certain conditions, such as, a minimum holding period of one year from the date of issue of IDRs and such IDR qualifying as an infrequently traded security on the stock exchange(s) in India. This regulatory position has now being modified by SEBI and RBI to provide for limited two-way fungibility for IDRs, similar to the fungibility available in case of an american depository receipt (ADR) or global depository receipt (GDR).

BACKGROUND

An IDR is basically a security listed on an Indian stock exchange, with its underlying being a listed security of a foreign incorporated and listed entity. The introduction of an IDR in the Indian securities market and the legal framework governing them was put in place with an objective to facilitate capital raising by foreign investors from domestic market, at the same time providing domestic investors an opportunity to make investments in securities of well-recognised multinational companies listed on developed markets. Till date, there is only one foreign company namely Standard Chartered Bank, Plc whose IDRs have been listed on an Indian stock exchange.

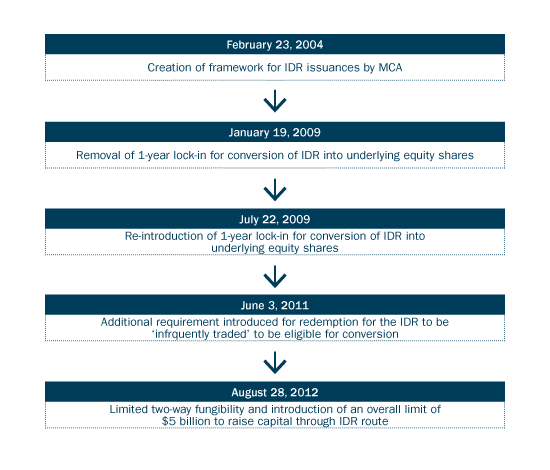

The regulatory position with respect to IDRs has been evolving ever since the regulatory framework governing IDR was introduced by the Ministry of Corporate Affairs (MCA) in the year 2004. The following figure traces the series of regulatory changes with respect to redemption of IDR:

Figure 1: Evolution of regulatory framework governing fungibility of IDR

The erstwhile Indian regulatory framework allowed only redemption / conversion of IDR into the underlying foreign security after fulfilling the prescribed conditions. The regulatory change would now enable even conversion of equity shares of a foreign issuer into IDR, to the extent of IDRs that have been redeemed / converted into underlying shares and sold.

KEY CHANGES INTRODUCED

The regulatory development allowing limited two-way fungibility flows from the announcement made by the then finance minister in his budget speech earlier this year. The following are some of the key highlights of this regulatory development:

-

Redemption / conversion of IDRs into equity shares

Redemption capped to the extent of 25% of originally issued IDR in a financial year

The circulars have now put in place a cap of 25% of the originally issued IDR as a maximum limit for redemption/conversion in a given financial year. This limit means that in any given financial year not more than 25% of the originally issued IDR may be redeemed/ converted into underlying equity shares of the foreign issuer whose IDRs are listed, subject to the requirement of holding such IDRs for a period of atleast one year from their issuance. Prior to this regulatory change, there was no ceiling on the number of IDRs that could be redeemed / converted into equity shares subject to fulfillment of eligibility criteria (discussed below). Introduction of this ceiling in light of allowing limited two-way fungibility appears to be logical so that the IDR market is not adversely impacted due to substantial redemptions.

Eligibility criteria for redemption/conversion

a) Minimum period of holding: One of the pre-requisite for redemption of IDRs into underlying equity shares is expiry of one year from the date of issue of IDRs (the “Lock-in Period”).2 The recent circulars have retained this eligibility criterion of minimum holding period of at least one year from the date of issue of IDR as prescribed in RBI circular3 to be eligible for redemption/conversion of IDR into underlying equity shares.

b) No requirement of IDR to be ‘infrequently traded’: SEBI vide its circular dated June 3, 2011 had prescribed an additional requirement for IDRs to be ‘infrequently traded’4 on stock exchange(s) in addition to the requirement of Lock-in Period for the IDRs to be eligible for redemption. This requirement for an IDR to be ‘infrequently traded’ has now been removed as SEBI has now rescinded its earlier circular dated June 3, 2011. This earlier SEBI circular was discussed in detail in our hotline titled “SEBI takes a U-turn: Limited Opportunity for Redemption of IDRs”.

In this regard, our firm on behalf of many investors had made representation to SEBI for removal of this requirement which restricted the ability of IDR holders to freely redeem their IDRs into the underlying equity shares even after the expiry of the statutory lock-in period of one year.

The removal of this requirement comes as a big relief to the investors looking to exit which were hitherto restricted because of this requirement.

Implication : The regulatory change of allowing two-way fungibility is a welcome move in the right direction towards increasing the viability of IDRs in the Indian markets. Additionally, the removal of requirement for an IDR to be ‘infrequently traded’ would go a long way in providing the required impetus to the IDR market.

-

Conversion of equity shares of the foreign issuer into IDR allowed to a limited extent

The regulatory framework governing IDR now enable conversion of equity shares into IDR which was previously not allowed. Such conversion would be limited to the pool of IDRs which were redeemed / converted into underlying equity shares by the original holders of IDRs. This condition appears to have been borrowed from the ADR/GDR guidelines which allow dual fungibility to the extent of headroom created through redemption of these depositary receipts and thus creates a level playing field from a regulatory perspective between the ADRs/GDRs and the IDRs.

-

USD 5 billion capital raising limit introduced for raising capital through IDR route

RBI has now put in place an overall limit of $5 billion for raising of capital through issuance of IDR. Although a separate limit in itself, this limit is similar to the limit which exists for FIIs investing in debt securities. Adherence to this limit will be monitored by SEBI.

Implication: Until now there was no cap on the overall amount that could have been raised under IDR issuances. The now prescribed overall cap of USD 5 billion through the IDR route appears sufficient for the time being considering that only one foreign issuer has used this route to raise capital till date from the Indian markets.

The rationale for introducing such a limit could be to cap the amount foreign companies may raise from domestic market as well as to cap outflow of capital through IDR issuances and/or to address systematic risk. However, such externally forced artificial limits are not efficiency-enhancing. Therefore, going forward this limit should gradually be done away with or at least be continuously expanded in order to accommodate the capital raising needs of businesses.

-

Implications on holders of underlying equity shares post redemption/conversion of IDR

It is important to note that the recent RBI circular continues with the requirement to comply with condition enumerated in regulation 7 of the earlier circular dated July 22, 2009 which provides the guidelines for holding underlying equity shares of the issuing company after redemption of IDRs by listed Indian companies, domestic mutual funds and other persons resident in India.

TAX IMPLICATIONS

Presently, there are no specific tax provisions under the Income-tax Act, 1961 with respect to tax implications at the time of redemption of IDRs into underlying equity shares. While SEBI and RBI have provided for limited two way fungibility, there exists no provision providing incentives under the tax laws to make the IDR regime attractive, viz, (i) any gains arising on redemptions of IDR into the underlying equity shares if not specifically exempt would lead to a situation of the holder being subjected to tax in the absence of any realised gains and hence making a redemption unattractive (ii) dividends received would be subject to tax as income from other sources and taxed at the regular tax rates applicable to the tax payer.

CONCLUSION

The rise of global finance has removed geographic boundaries for companies enabling them to raise capital in markets across the world. Issuance of depository receipts is an innovative mechanism especially for companies who are targeting to raise capital from a market other than the market of their primary listing.

Depository receipts provide mutual benefits to issuers, investors as well as to the host market. Companies get to raise capital from willing investors, diversify their investor base and fulfill strategic objective such as for e.g. brand recognition. Investors get to invest in companies in which they otherwise could not have easily invested, diversifying their portfolio in the process. Ultimately, markets tend to become more efficient as increased access for investors through multiple listings enhances liquidity, and improves price-discovery.

The regulatory change brought about to allow limited two-way fungibility is a step in the right direction, and it should make IDRs relatively more marketable. However, the results are more likely to be visible only when the other challenges faced by the Indian capital market are addressed.

– Aditya Shukla, Ruchi Biyani & Vyapak Desai

You can direct your queries or comments to the authors

1 Reserve Bank of India A. P. (DIR Series) Circular No. 19 (August 28 2012) and SEBI Circular No. CIR/CFD/DIL/10/2012 (August 28, 2012).

2 Reserve Bank of India A. P. (DIR Series) Circular No. 19 (July 22, 2009).

3 Reserve Bank of India A. P. (DIR Series) Circular No. 19 (August 28 2012) (para 2(i)).

4 The SEBI Circular (Circular No. CIR/CFD/DIL/3/2011 dated June 3, 2011) explains ‘infrequently traded’ to mean that the annualized trading turnover in IDRs during the six calendar months immediately preceding the month of redemption is less than five percent of the listed IDRs.

Disclaimer

The contents of this hotline should not be construed as legal opinion. View detailed disclaimer.

Research PapersMergers & Acquisitions New Age of Franchising Life Sciences 2025 |

Research Articles |

AudioCCI’s Deal Value Test Securities Market Regulator’s Continued Quest Against “Unfiltered” Financial Advice Digital Lending - Part 1 - What's New with NBFC P2Ps |

NDA ConnectConnect with us at events, |

NDA Hotline |