Deal DestinationMay 21, 2020 Demystifying ‘Real Estate Platforms’

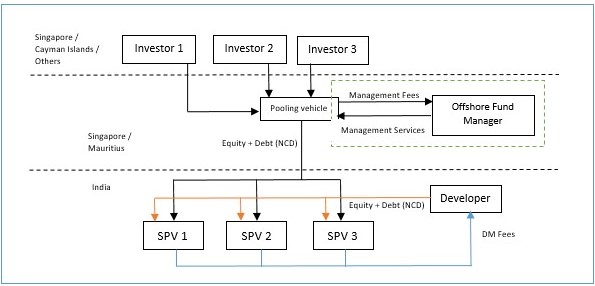

There was once a saying that you never lose in Indian real estate, only cash flow mismatches. While the sector has gone through its own challenges, there are still pockets within the sector which hold great promise for offshore investors. Amongst the three P’s of real estate, being property, price and promoter (founder), it is indubitably the promoter that holds the promise to a successful real estate venture. If the partner or promoter is ethical and commercially sound, real estate funds have made good money even in depressed markets. Hence, fund managers decided to partner with reputed partners with a proven track record, to create managed account structures of sorts, also called as “Developer Platforms” or “RE Platforms”. The Developer Platforms differ from conventional fund structures inasmuch as there are no GP – LP relationships. More often than not, one may find reputed LPs directly establishing such platforms with developers as against investing in blind pools or managed accounts with financial sponsors. Considering the growing importance and interest that such platforms have garnered from global financial investors, and developers alike, it may be pertinent to note some of the key issues that one should keep in mind for such platforms. STRUCTURE CONSIDERATIONS· Platform structure The structure of the platform is important and can be in the nature of (a) a pooling vehicle investing in the platform entities directly along with the developer, where the developer also acts as the development manager, or (b) where the developer in addition to investing in the platform entities and acting as the developer, is also the fund manager of the offshore pooling vehicle.

· Choice of jurisdiction Setting up the pooling vehicle in a jurisdiction that is favourable from an ease of doing business and corporate compliances, and has a favourable double tax avoidance agreement with India is of utmost importance in setting up RE platforms. This ensures that the costs of compliance are low and the returns are not severely impacted by tax leakages in India or the jurisdiction in which the fund is set up. Singapore and Mauritius are preferred jurisdictions since the tax rates (including withholding tax rates) in India are low for both jurisdictions, for both equity and debt. · Choice of instruments Another critical aspect of the RE Platform is the choice of instruments used by the pooling vehicle for investments into India. The Indian exchange control regulations limit investment by foreign investors to equity shares or compulsorily convertible instruments under the direct investment route. In addition, portfolio investors registered with the securities regulator (SEBI) can also invest in non-convertible debentures for extraction of cash from the portfolios in a tax efficient manner. This is also determined based on the portfolio of assets (see below). The choice of instruments may also become pertinent from a consolidation of the investment perspective for the investors and the developer. · Choice and parameters of portfolio The RE Platform may concentrate on commercial real estate (like malls, office spaces) or on residential real estate or a mix of both. The instruments and the terms of the instruments would depend largely on the mix of the portfolio. In case of commercial assets, i.e. a yield model, investors prefer debt instruments like non-convertible debentures which permit them to extract cash regularly. On the other hand, in cases of residential projects, where investors look for equity upside, structured debt instruments which can be redeemed periodically at premiums are preferred. Usually, a mix of debt and equity is preferred, and the debt-equity ratio is a determinant of the portfolio. Further, for platform for future projects, base parameters, or conditions that would need to be satisfied by a project for the developer to present the opportunity to the platform are also laid down in detail. These conditions could include geographical restrictions, minimum return / IRR components, minimum or maximum cost of development, and the nature of the project (commercial – residential or a mix of the two in a ratio). This ensures that the platform evaluates the feasibility and desirability of only projects which satisfy base conditions which the investors are interested in. On the other hand, this permits the developers to consider projects which do not meet these minimum conditions outside of the platform as well. In addition, the RE Platform also needs to evaluate the kind of investment opportunities it intends to explore. These could be in the form of outright acquisition of land and development, joint-development agreement with land owners or development of specialized commercial real estate (such as IT Parks and SEZ) on land leased by governmental authorities. GOVERNANCE RELATED· Decision making process One of the most heavily negotiated clauses in a platform deal involves the overall decision making process of the RE Platform. This includes (a) investment decision with respect to the projects to invest in; and (b) day to day operations of the portfolio companies. With respect to investment decisions, it is best to lay down in as much detail as possible, the entire process for the decision to invest in a project. This commences with the developer presenting an initial bare bones investment proposal to the decision making body of the RE Platform, followed by a detailed diligence and investment proposal (if the initial proposal is accepted). Finally, based on the detailed information, the decision-making body determines if they intend to proceed with the investment or not. The investment decisions usually are required to be swift to ensure that potential opportunities are not missed due to an extended decision making process. With respect to the day-to-day operations, RE Platforms prefer to have a committee (akin to a committee of the board of directors) which oversee and monitor the performance of each of the portfolio companies. Any decision of the board of directors or similar governing body would be based on the advice of such committee in most cases. Significant investors (holding say, 10% of the entire RE Platform) may ask for standard reserved matters as well on various activities of the RE Platform and / or the portfolio companies. Couple of other aspects to be borne in mind with respect to the decision making process of the RE Platform are as following:

· Deadlock mechanism Closely linked to the previous point, the chances of a deadlock in a RE Platform are high, considering the numerous decisions that are required to be taken by the RE Platform on a regular basis, including with respect to each portfolio project. To ensure that any such deadlock does not impact the overall RE Platform (unless the deadlock is over an issue encompassing the entire platform), one may carefully consider whether deadlock in one platform entity will result in deadlock across the entire platform, or will remain ringfenced to just that platform entity. Private equity funds generally prefer that a deadlock in any platform entity is a platform level deadlock. Considering the long-standing relation between the parties, escalating the matter to senior level management of the parties involved should be preferred, and then to industry experts as commercial arbitrators. Further, in the event that there is no resolution to the deadlock, the implications of such deadlock may range from buy-sell events to appointing a third party manager. · Developer’s non-compete and exclusivity An important aspect of the RE Platform is to ensure continuity of good projects to be provided to the RE Platform. To ensure this, investors put in a few restrictions on the developer. These are usually two-pronged. Firstly, investors prefer to put non-compete restrictions on the developer. This is generally limited to a defined geographical area or project type. For instance, the developer is restricted from launching any projects outside the RE Platform for a defined city or a defined radius around any existing project of the RE Platform. Further, project type restrictions could be in the form of luxury / affordable housing segments (depending on the RE Platform’s focus) or type of commercial real estate (depending on the RE Platform’s focus again). Secondly, the RE Platform usually requires the developer to provide an exclusivity to the RE Platform and the investors there. However, while such exclusivity was noted in the first few platform transactions, such exclusivity has been resisted by developers. Such exclusivity provisions have been replaced with right of first refusal (ROFR) being offered to the RE Platform. Accordingly, the developer is required to first offer any potential investment opportunity to the RE Platform, and in the event that the RE Platform rejects or decides not to invest in the project, the developer may explore the opportunity with other parties. The interplay between the non-compete and the ROFR needs to be carefully evaluated and agreed between parties. · Transfer of interests and investor defaults Since the developer and the investors establish the RE Platform based on comfort with each other, akin to a joint venture, any transfer of the interests in the RE Platform is an extremely important aspect to be considered in detail. Generally, any transfer is subject to a right of first offer (ROFO) to the other investors. Considering the nature of the investment, a ROFO may also be followed by a right to match. In addition, the other members of the RE Platform (including the developer) may also want rights to ensure that the incoming investor is acceptable to each of them to ensure the sustainable nature of the RE Platform. The transfer of interests to a competitor is also restricted, and competitor could include any person in ownership or development / construction of real estate. Equally important is to have detailed provisions with respect to a default of an investor in case of any capital call. In such cases, where the RE Platform has agreed to invest in a potential project, and each of the investors need to invest in ratio of their partnership interest. If any investor is unable to invest, the other investors and the developer are permitted to cover for the non-investing / defaulting investor’s portion. In such cases, ensuring that the returns are also tracked accordingly becomes important. Structures such as the Variable Capital Company (Singapore) and Protected Cell Company (Mauritius) may be helpful. · Developer defaults As opposed to any other joint venture / inter-se arrangement between shareholders of a company, various aspects need to be considered in any default in an RE Platform by the developer. These are (i) platform level vs project specific default, and (ii) default as a shareholder vs default as a developer. Defaults on a platform level relate to overall activities of the developer, such as the developer being guilty of any offence or fraud, initiation of insolvency proceedings against the developer or any of its controlling entities and adverse impact on the brand / tradename of the developer. On the other hand, project level defaults include breach of obligations of the developer under the relevant platform project documents, inability / failure to meet construction or sales milestones and inability of the developer to fund the project pursuant to any capital requirements. The implications of either kind of default also needs to be correspondingly determined. Termination of the development management / project management agreement, ability to sell the relevant project(s) or replacing the development manager / project manager with another development manager / project manager; in either case for the relevant project or for the entire RE Platform are corresponding consequences of the default. In addition, the default of the developer in its capacity as a ‘shareholder’ and as a ‘developer’ also needs to be evaluated closely. Default as a shareholder may impact returns of the developer solely as a shareholder, and the development / project management arrangement and the fees payable thereunder could continue as usual. On the other hand, default as a ‘developer’ could result in termination of the development / project management agreement, while the rights of the developer as a shareholder may continue. In either of the cases above, the branding of the project is extremely critical and needs to be evaluated in depth (see below). DEVELOPMENT / PROJECT MANAGEMENT RELATED· Role and obligations of the developer The role and the obligation of the developer should be set out clearly and in detail. The requirement of ensuring all approvals for the project is in order, the development and construction of the project is in accordance with the local and municipal laws, the costs of development are within the permitted limits and marketing and branding responsibilities should be laid out in detail. · Development / project management fee The development / project management fee is a fee provided to the developer for the development / construction (in case of under construction projects) or the project management fees (in case of ready assets). The fee is a part of the construction cost for the project, and hence is paid to the developer prior to, and over and above the returns made by the developer in its capacity as a shareholder. The fee can be a fixed rate per square foot, or linked to the construction costs / returns / sale proceeds of the project. Usually, the fee is structured as a mix of a fee linked to construction costs or fixed fee per square foot (to compensate the developer for its costs), and a variable linked to returns / sale proceeds (to incentivise the developer for additional recoveries). The fees are generally linked to the kind of project (luxury, mid-market or affordable housing) and the asset class (commercial / residential). · Branding and marketing One of the most critical aspects of the RE Platform, and the reason why the investors chose to partner with the developer is the branding of the developer. The investor takes comfort in reputed names with good developmental experience and record, and relies on the same for the development. In case of any default by the developer (on a project or a platform level), and corresponding removal of the developer as the ‘developer of the project’ becomes a cause of concern from a branding perspective. While the developer may require that the project be rechristened or re-branded with the brand of the incoming / new developer, the investors may not be comfortable with changing the branding of the project since it may impact the marketability of the project, in addition to bringing major changes overall to the project. While the issues and challenges faced in setting up RE Platforms are varied and unique in every transaction, the issues mentioned above are common and are faced in some form or the other in all platforms. It would be prudent for an investor and the developer to discuss and agree to some of these aspects upfront at the time of the term sheet itself, rather than these issues cropping up later. DisclaimerThe contents of this hotline should not be construed as legal opinion. View detailed disclaimer. |

|

There was once a saying that you never lose in Indian real estate, only cash flow mismatches. While the sector has gone through its own challenges, there are still pockets within the sector which hold great promise for offshore investors. Amongst the three P’s of real estate, being property, price and promoter (founder), it is indubitably the promoter that holds the promise to a successful real estate venture. If the partner or promoter is ethical and commercially sound, real estate funds have made good money even in depressed markets. Hence, fund managers decided to partner with reputed partners with a proven track record, to create managed account structures of sorts, also called as “Developer Platforms” or “RE Platforms”.

The Developer Platforms differ from conventional fund structures inasmuch as there are no GP – LP relationships. More often than not, one may find reputed LPs directly establishing such platforms with developers as against investing in blind pools or managed accounts with financial sponsors.

Considering the growing importance and interest that such platforms have garnered from global financial investors, and developers alike, it may be pertinent to note some of the key issues that one should keep in mind for such platforms.

STRUCTURE CONSIDERATIONS

· Platform structure

The structure of the platform is important and can be in the nature of (a) a pooling vehicle investing in the platform entities directly along with the developer, where the developer also acts as the development manager, or (b) where the developer in addition to investing in the platform entities and acting as the developer, is also the fund manager of the offshore pooling vehicle.

· Choice of jurisdiction

Setting up the pooling vehicle in a jurisdiction that is favourable from an ease of doing business and corporate compliances, and has a favourable double tax avoidance agreement with India is of utmost importance in setting up RE platforms. This ensures that the costs of compliance are low and the returns are not severely impacted by tax leakages in India or the jurisdiction in which the fund is set up. Singapore and Mauritius are preferred jurisdictions since the tax rates (including withholding tax rates) in India are low for both jurisdictions, for both equity and debt.

· Choice of instruments

Another critical aspect of the RE Platform is the choice of instruments used by the pooling vehicle for investments into India. The Indian exchange control regulations limit investment by foreign investors to equity shares or compulsorily convertible instruments under the direct investment route. In addition, portfolio investors registered with the securities regulator (SEBI) can also invest in non-convertible debentures for extraction of cash from the portfolios in a tax efficient manner. This is also determined based on the portfolio of assets (see below). The choice of instruments may also become pertinent from a consolidation of the investment perspective for the investors and the developer.

· Choice and parameters of portfolio

The RE Platform may concentrate on commercial real estate (like malls, office spaces) or on residential real estate or a mix of both. The instruments and the terms of the instruments would depend largely on the mix of the portfolio. In case of commercial assets, i.e. a yield model, investors prefer debt instruments like non-convertible debentures which permit them to extract cash regularly. On the other hand, in cases of residential projects, where investors look for equity upside, structured debt instruments which can be redeemed periodically at premiums are preferred. Usually, a mix of debt and equity is preferred, and the debt-equity ratio is a determinant of the portfolio.

Further, for platform for future projects, base parameters, or conditions that would need to be satisfied by a project for the developer to present the opportunity to the platform are also laid down in detail. These conditions could include geographical restrictions, minimum return / IRR components, minimum or maximum cost of development, and the nature of the project (commercial – residential or a mix of the two in a ratio). This ensures that the platform evaluates the feasibility and desirability of only projects which satisfy base conditions which the investors are interested in. On the other hand, this permits the developers to consider projects which do not meet these minimum conditions outside of the platform as well.

In addition, the RE Platform also needs to evaluate the kind of investment opportunities it intends to explore. These could be in the form of outright acquisition of land and development, joint-development agreement with land owners or development of specialized commercial real estate (such as IT Parks and SEZ) on land leased by governmental authorities.

GOVERNANCE RELATED

· Decision making process

One of the most heavily negotiated clauses in a platform deal involves the overall decision making process of the RE Platform. This includes (a) investment decision with respect to the projects to invest in; and (b) day to day operations of the portfolio companies.

With respect to investment decisions, it is best to lay down in as much detail as possible, the entire process for the decision to invest in a project. This commences with the developer presenting an initial bare bones investment proposal to the decision making body of the RE Platform, followed by a detailed diligence and investment proposal (if the initial proposal is accepted). Finally, based on the detailed information, the decision-making body determines if they intend to proceed with the investment or not. The investment decisions usually are required to be swift to ensure that potential opportunities are not missed due to an extended decision making process.

With respect to the day-to-day operations, RE Platforms prefer to have a committee (akin to a committee of the board of directors) which oversee and monitor the performance of each of the portfolio companies. Any decision of the board of directors or similar governing body would be based on the advice of such committee in most cases. Significant investors (holding say, 10% of the entire RE Platform) may ask for standard reserved matters as well on various activities of the RE Platform and / or the portfolio companies.

Couple of other aspects to be borne in mind with respect to the decision making process of the RE Platform are as following:

- Developer’s role

The role of the developer as a sponsor to the entire RE Platform and its role as a developer to the portfolio projects need to be segregated, and the ‘developer’ hat should not be given a substantial role to play in the decision making process of the RE Platform. Care should be taken to ensure that the document covers this. - Investment decisions

In case of multiplicity of investors in the RE Platform, it should be ensured that no single investor has the ability to block decisions on whether to invest in a potential project. This ensures that no investor has the right to restrict the RE Platform from investing in a project, solely due to reasons attributable to it (for instance, inability to arrange / call down for funds from the limited partners in a given time frame).

· Deadlock mechanism

Closely linked to the previous point, the chances of a deadlock in a RE Platform are high, considering the numerous decisions that are required to be taken by the RE Platform on a regular basis, including with respect to each portfolio project. To ensure that any such deadlock does not impact the overall RE Platform (unless the deadlock is over an issue encompassing the entire platform), one may carefully consider whether deadlock in one platform entity will result in deadlock across the entire platform, or will remain ringfenced to just that platform entity. Private equity funds generally prefer that a deadlock in any platform entity is a platform level deadlock. Considering the long-standing relation between the parties, escalating the matter to senior level management of the parties involved should be preferred, and then to industry experts as commercial arbitrators. Further, in the event that there is no resolution to the deadlock, the implications of such deadlock may range from buy-sell events to appointing a third party manager.

· Developer’s non-compete and exclusivity

An important aspect of the RE Platform is to ensure continuity of good projects to be provided to the RE Platform. To ensure this, investors put in a few restrictions on the developer. These are usually two-pronged.

Firstly, investors prefer to put non-compete restrictions on the developer. This is generally limited to a defined geographical area or project type. For instance, the developer is restricted from launching any projects outside the RE Platform for a defined city or a defined radius around any existing project of the RE Platform. Further, project type restrictions could be in the form of luxury / affordable housing segments (depending on the RE Platform’s focus) or type of commercial real estate (depending on the RE Platform’s focus again).

Secondly, the RE Platform usually requires the developer to provide an exclusivity to the RE Platform and the investors there. However, while such exclusivity was noted in the first few platform transactions, such exclusivity has been resisted by developers. Such exclusivity provisions have been replaced with right of first refusal (ROFR) being offered to the RE Platform. Accordingly, the developer is required to first offer any potential investment opportunity to the RE Platform, and in the event that the RE Platform rejects or decides not to invest in the project, the developer may explore the opportunity with other parties. The interplay between the non-compete and the ROFR needs to be carefully evaluated and agreed between parties.

· Transfer of interests and investor defaults

Since the developer and the investors establish the RE Platform based on comfort with each other, akin to a joint venture, any transfer of the interests in the RE Platform is an extremely important aspect to be considered in detail. Generally, any transfer is subject to a right of first offer (ROFO) to the other investors. Considering the nature of the investment, a ROFO may also be followed by a right to match. In addition, the other members of the RE Platform (including the developer) may also want rights to ensure that the incoming investor is acceptable to each of them to ensure the sustainable nature of the RE Platform. The transfer of interests to a competitor is also restricted, and competitor could include any person in ownership or development / construction of real estate.

Equally important is to have detailed provisions with respect to a default of an investor in case of any capital call. In such cases, where the RE Platform has agreed to invest in a potential project, and each of the investors need to invest in ratio of their partnership interest. If any investor is unable to invest, the other investors and the developer are permitted to cover for the non-investing / defaulting investor’s portion. In such cases, ensuring that the returns are also tracked accordingly becomes important. Structures such as the Variable Capital Company (Singapore) and Protected Cell Company (Mauritius) may be helpful.

· Developer defaults

As opposed to any other joint venture / inter-se arrangement between shareholders of a company, various aspects need to be considered in any default in an RE Platform by the developer. These are (i) platform level vs project specific default, and (ii) default as a shareholder vs default as a developer.

Defaults on a platform level relate to overall activities of the developer, such as the developer being guilty of any offence or fraud, initiation of insolvency proceedings against the developer or any of its controlling entities and adverse impact on the brand / tradename of the developer. On the other hand, project level defaults include breach of obligations of the developer under the relevant platform project documents, inability / failure to meet construction or sales milestones and inability of the developer to fund the project pursuant to any capital requirements. The implications of either kind of default also needs to be correspondingly determined. Termination of the development management / project management agreement, ability to sell the relevant project(s) or replacing the development manager / project manager with another development manager / project manager; in either case for the relevant project or for the entire RE Platform are corresponding consequences of the default.

In addition, the default of the developer in its capacity as a ‘shareholder’ and as a ‘developer’ also needs to be evaluated closely. Default as a shareholder may impact returns of the developer solely as a shareholder, and the development / project management arrangement and the fees payable thereunder could continue as usual. On the other hand, default as a ‘developer’ could result in termination of the development / project management agreement, while the rights of the developer as a shareholder may continue.

In either of the cases above, the branding of the project is extremely critical and needs to be evaluated in depth (see below).

DEVELOPMENT / PROJECT MANAGEMENT RELATED

· Role and obligations of the developer

The role and the obligation of the developer should be set out clearly and in detail. The requirement of ensuring all approvals for the project is in order, the development and construction of the project is in accordance with the local and municipal laws, the costs of development are within the permitted limits and marketing and branding responsibilities should be laid out in detail.

· Development / project management fee

The development / project management fee is a fee provided to the developer for the development / construction (in case of under construction projects) or the project management fees (in case of ready assets). The fee is a part of the construction cost for the project, and hence is paid to the developer prior to, and over and above the returns made by the developer in its capacity as a shareholder. The fee can be a fixed rate per square foot, or linked to the construction costs / returns / sale proceeds of the project. Usually, the fee is structured as a mix of a fee linked to construction costs or fixed fee per square foot (to compensate the developer for its costs), and a variable linked to returns / sale proceeds (to incentivise the developer for additional recoveries). The fees are generally linked to the kind of project (luxury, mid-market or affordable housing) and the asset class (commercial / residential).

· Branding and marketing

One of the most critical aspects of the RE Platform, and the reason why the investors chose to partner with the developer is the branding of the developer. The investor takes comfort in reputed names with good developmental experience and record, and relies on the same for the development. In case of any default by the developer (on a project or a platform level), and corresponding removal of the developer as the ‘developer of the project’ becomes a cause of concern from a branding perspective. While the developer may require that the project be rechristened or re-branded with the brand of the incoming / new developer, the investors may not be comfortable with changing the branding of the project since it may impact the marketability of the project, in addition to bringing major changes overall to the project.

While the issues and challenges faced in setting up RE Platforms are varied and unique in every transaction, the issues mentioned above are common and are faced in some form or the other in all platforms. It would be prudent for an investor and the developer to discuss and agree to some of these aspects upfront at the time of the term sheet itself, rather than these issues cropping up later.

Disclaimer

The contents of this hotline should not be construed as legal opinion. View detailed disclaimer.

Research PapersMergers & Acquisitions New Age of Franchising Life Sciences 2025 |

Research Articles |

AudioCCI’s Deal Value Test Securities Market Regulator’s Continued Quest Against “Unfiltered” Financial Advice Digital Lending - Part 1 - What's New with NBFC P2Ps |

NDA ConnectConnect with us at events, |

NDA Hotline |