Investment Funds: Monthly DigestOctober 23, 2023 SEC Strengthens Norms for PE FundsBACKGROUNDOn August 23, 2023, the Securities and Exchange Commission (“SEC”) adopted its final rule on private fund advisors1 (“Final Rule”) ushering in five new rules and certain amendments to existing regulations in furtherance of bolstering investor protection. The Final Rule addresses key aspects of fund governance including but not limited to preferential treatment of certain investors, filing of annual audits, submission of quarterly reports, contours on adviser-led secondaries, and enhanced record-keeping provisions. Governance norms in private funds (including AIFs in India) are derived from worldwide practices, especially when monies are being raised from global investors. In this monthly digest, we analyze the new changes ushered in by the SEC and undertake a comparative analysis of the same with the prevailing position in India. Nothing contained in this article should be construed as legal advise including on US laws. This analysis has been done on the basis of market research and experience. We disavow any errors and in specific pertaining to legal accuracy or current status of US laws contained in this article. INTRODUCTION TO THE US FUNDS INDUSTRYA general overview of the US investment funds industry under the Investment Advisors Act, 1940 (“Advisors Act”) is provided below.

NEW RULES INTRODUCED BY THE SECTabulated below is a snapshot of the new rules adopted by the SEC in relation to investment advisers to private funds.

Provided below is a comparative table of the provisions covered under the Final Rules and the extant provisions applicable to alternative investment funds (“AIFs”) under various Securities and Exchange Board of India (“SEBI”) regulations and other applicable laws.

It may be observed from the table above that the AIF Regulations in the current form place equivalent, if not more restrictive measures on all AIFs (without many practicable exemptions, unlike in the US) in order to ensure adequate investor protection. Herein, it may be noted that, as opposed to necessitating investor consent (under the Advisors Act) for certain actions, the same has been outright prohibited by SEBI for AIFs. For example, while the SEC rules permit the fund to obtain line of credit from a client / investor,35 the AIF Regulations places a prohibition on AIFs from undertaking any leverage. Interestingly, the Final Rules have introduced some level of parity between the Indian regulations and its American counterparts- especially in record keeping (however, the AIF Regulations tend to require a greater compliance burden on GPs). For example, the AIF Regulations obligate AIFs to provide information with respect to material risks to investors in addition to purely financial information. CONCLUSIONThe AIF Regulations substantively address the new rules proposed by the SEC. It may appear that the SEC is playing catch-up when it comes to investor protection as compared to SEBI’s AIF Regulations. Nevertheless, the recent SEC move may be examined from two lenses-

Irrespective of which perspective one prefers, the regulatory dilemma persists i.e. the regulator has to ensure adequate investor protection while encouraging capital development. While upkeeping this fragile balance, it is interesting to observe that the SEC has adopted the Final Rules which bolsters investor protection –with the increased cost of additional compliance burden.

You can direct your queries or comments to the authors. 1 Private Fund Advisers; Documentation of Registered Investment Adviser Compliance, Release No. IA-6383; File No. S7-03-22 https://www.govinfo.gov/content/pkg/FR-2023-09-14/pdf/2023-18660.pdf 2 Fairness opinion and summary note 3 Please refer to the table below for the specific activities under the preferential treatment rule 4 Please refer to the table below for the specific activities under the preferential treatment rule 5 Please refer to the table below for the specific activities under the restricted activities rule 6 Please refer to the table below for the specific activities under the restricted activities rule 7 Rule 211(h)(2)-1 8 Clause 11, SEBI (Alternative Dispute Resolution Mechanism) (Amendment) Regulations, 2023 9 Regulation 22 (c), AIF Regulations 10 Master Circular for AIFs, SEBI circular SEBI/HO/AFD/PoD1/P/CIR/2023/130, July 31, 2023 (“AIF Master Circular”) 11 Consultation paper on proposal with respect to pro-rata and pari-passu rights of investors of AIFs, May 23, 2023 12 Regulation 15 (1)(b), AIF Regulations 13 Regulation 3(4)(b), AIF Regulations & Regulation 16(1)(c), AIF Regulations 14 Regulation 22 (g)(iii), AIF Regulations 15 Regulation 3(4)(c), AIF Regulations 16 Rule 211(h)(2)-3 17 Rule 206(4)-10 18 180 days in case of a fund of funds. 19 Regulation 22(g) and regulation 22(j), AIF Regulations 20 Rule 211(h)(1)-2 21 Regulation 22(b), AIF Regulations 22 Regulation 22(a), AIF Regulations 23 Quarterly reporting format, available at: https://www.ivca.in/regulatory-reports-sebi-circular 24 Rule 211(h)(2)-2 25 Regulation 29A, AIF Regulations 26 Modalities for launching Liquidation Scheme and for distributing the investments of AIFs in-specie, SEBI circular SEBI/HO/AFD/PoD-I/P/CIR/2023/098 dated June 21, 2023 27 Rule 204-2 28 Stewardship code, AIF Master Circular 29 Regulation 27 (1)(e), AIF Regulations 30 Regulation 27 (1)(d), AIF Regulations 31 Regulation 27 (1)(a), AIF Regulations 32 Regulation 30 and regulation 32, AIF Regulations 33 Rule 206(4)-7(b) 34 Clause 2.4, AIF Master Circular 35 Provided that it obtains a majority consent of investors and provides all investors with a note capturing the material terms of the credit line 36 Private funds prepare to spend billions on compliance after SEC rule, Financial Times https://www.ft.com/content/6d39f967-e141-418c-aef0-76bb337c64ba DisclaimerThe contents of this hotline should not be construed as legal opinion. View detailed disclaimer. |

|

BACKGROUND

On August 23, 2023, the Securities and Exchange Commission (“SEC”) adopted its final rule on private fund advisors1 (“Final Rule”) ushering in five new rules and certain amendments to existing regulations in furtherance of bolstering investor protection. The Final Rule addresses key aspects of fund governance including but not limited to preferential treatment of certain investors, filing of annual audits, submission of quarterly reports, contours on adviser-led secondaries, and enhanced record-keeping provisions.

Governance norms in private funds (including AIFs in India) are derived from worldwide practices, especially when monies are being raised from global investors. In this monthly digest, we analyze the new changes ushered in by the SEC and undertake a comparative analysis of the same with the prevailing position in India.

Nothing contained in this article should be construed as legal advise including on US laws. This analysis has been done on the basis of market research and experience. We disavow any errors and in specific pertaining to legal accuracy or current status of US laws contained in this article.

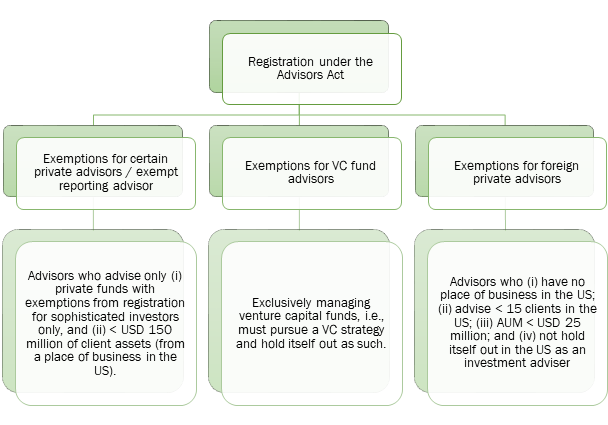

INTRODUCTION TO THE US FUNDS INDUSTRY

A general overview of the US investment funds industry under the Investment Advisors Act, 1940 (“Advisors Act”) is provided below.

NEW RULES INTRODUCED BY THE SEC

Tabulated below is a snapshot of the new rules adopted by the SEC in relation to investment advisers to private funds.

|

Rule |

Any investment adviser |

Registered investment adviser |

Grandfathered / Legacy Status |

Written notice to investors |

Majority consent of unrelated investors |

Additional documents to investors |

|

Quarterly statement rule |

❌ |

☺ |

❌ |

☺ |

❌ |

❌ |

|

Annual audits rule |

❌ |

☺ |

❌ |

☺ |

❌ |

❌ |

|

Adviser-led secondaries rule |

❌ |

☺ |

❌ |

☺ |

❌ |

☺2 |

|

Preferential treatment rule |

☺ |

- |

☺ |

-3 |

-4 |

❌ |

|

Restricted activities rule |

☺ |

- |

☺ |

-5 |

-6 |

❌ |

|

Bookkeeping rule amendments |

☺ |

- |

❌ |

☺ |

❌ |

❌ |

|

Compliance rule amendments |

☺ |

- |

❌ |

☺ |

❌ |

❌ |

Provided below is a comparative table of the provisions covered under the Final Rules and the extant provisions applicable to alternative investment funds (“AIFs”) under various Securities and Exchange Board of India (“SEBI”) regulations and other applicable laws.

|

New US Provisions |

Extant Indian Provisions |

|

Restricted Activities7 Investment advisors to a private fund are now required to:

|

Restricted Activities

Whereas Category III AIFs are permitted to utilize leverage provided that investors are provided certain additional SEBI mandated disclosures such as the overall level of leverage and level of leverage arising from derivatives.15 |

|

Preferential Treatment16 To ensure that the investors in a similar pool of assets or the same fund managed by an investment adviser are not treated unequally, the investment adviser has to ensure that:

The investment adviser ought to ensure that a written notice capturing the above information to both current and prospective investors. |

Preferential Treatment SEBI has recently released a consultation paper when seeks to ensure that the fund does not offer terms to any investors that would affect the pro-rata and pari-passu standing of all investors in the blind pool wherein certain differential economic rights may not be offered to select investors. The ramifications of mandating pro-rata / pari passu treatment of all investors are covered here. Currently, the template PPM necessitates the disclosure (illustrative) of the differential rights offered (if any). |

|

Private Fund Adviser Audits17 The investment adviser is obligated to ensure that every fund that it advises undertakes a financial audit and that such audited financial statements are distributed to its investors within 120 days of the fiscal year end18. The abovementioned annual audit is to be conducted by an independent public accountant and is to be prepared in accordance with US GAAP. |

Private Fund Adviser Audits AIFs are required to on an annual basis (within 180 days from year-end) provide investors with financial information of portfolio companies and material risks (and mitigation strategies) as week as undertake an annual audit by a qualified auditor.19 |

|

Quarterly Statements20 Investment advisers are required to, within the prescribed timelines, prepare and distribute quarterly statements for funds it advises that have two full fiscal quarters of operating results. This quarterly statement should, inter alia, contain the following:

It is to be noted that the above disclosures are to be made in plain and concise English. |

Quarterly Statements

|

|

Adviser-Led Secondaries24 For undertaking an adviser led secondary the investment adviser is required to:

|

Adviser-Led Secondaries The AIF Regulations are silent on IM-led secondaries, however, it provides for a liquidation scheme for holding unliquidated investments post the expiry of the AIF’s tenure.25 To ensure fairness in the transfer of unliquidated investments into the liquidation scheme, the AIF Regulations provides that the valuation of such unliquidated investments be done by two independent valuers and the AIF manager arrange for at least 25% bids for the value of such unliquidated investments.26 We have discussed the modalities of liquidation scheme in our previous digest here. |

|

Books and Records27 The extant recording keeping rules have been amended by the SEC to necessitate the preparation and retention following:

|

Books and Records The investment manager is obligated to maintain all the records specified by SEBI which include:

It is to be noted that SEBI has the right to inspect the AIF’s books of accounts and the onus is on the AIF (and its officers) to produce the same.32 We have also talked about the governance standards applicable to AIFs here. |

|

Compliance Procedures and Practices33 Presently, the investment advisers are required to annually review and document in writing the adequacy of policies and procedures adopted by the private fund pursuant to the Final Rules. |

Compliance Procedures and Practices The master circular for AIFs (“AIF Master Circular”) necessitates a legal audit of PPM to ensure that the AIF is in compliance with the AIF Regulations.34 |

It may be observed from the table above that the AIF Regulations in the current form place equivalent, if not more restrictive measures on all AIFs (without many practicable exemptions, unlike in the US) in order to ensure adequate investor protection. Herein, it may be noted that, as opposed to necessitating investor consent (under the Advisors Act) for certain actions, the same has been outright prohibited by SEBI for AIFs. For example, while the SEC rules permit the fund to obtain line of credit from a client / investor,35 the AIF Regulations places a prohibition on AIFs from undertaking any leverage.

Interestingly, the Final Rules have introduced some level of parity between the Indian regulations and its American counterparts- especially in record keeping (however, the AIF Regulations tend to require a greater compliance burden on GPs). For example, the AIF Regulations obligate AIFs to provide information with respect to material risks to investors in addition to purely financial information.

CONCLUSION

The AIF Regulations substantively address the new rules proposed by the SEC. It may appear that the SEC is playing catch-up when it comes to investor protection as compared to SEBI’s AIF Regulations. Nevertheless, the recent SEC move may be examined from two lenses-

-

From the perspective of investors, the move by the SEC is a step in the right direction wherein the regulator has put in place baseline investor protection measures that shall deter fraudulent practices by investment managers. The same was the need of the hour considering that the alternative investments industry now manages assets north of USD 25 trillion.

-

From the perspective of the investment managers, the Final Rules imposes additional compliance burden – to the tune of a billion dollars36 across the industry. The additional cost acts as a barrier to entry for emerging fund managers, has the potential to adversely impact the economics of smaller fund manager to a great extent, and may ultimately reduce the returns to the investors. The intended investors in such private funds are largely sophisticated investors who are capable of navigating the inherent complexities of such products and, therefore, a more light-touch regulatory regime should have been the norm.

Irrespective of which perspective one prefers, the regulatory dilemma persists i.e. the regulator has to ensure adequate investor protection while encouraging capital development. While upkeeping this fragile balance, it is interesting to observe that the SEC has adopted the Final Rules which bolsters investor protection –with the increased cost of additional compliance burden.

– Athul Kumar and Nandini Pathak

You can direct your queries or comments to the authors.

1 Private Fund Advisers; Documentation of Registered Investment Adviser Compliance, Release No. IA-6383; File No. S7-03-22

https://www.govinfo.gov/content/pkg/FR-2023-09-14/pdf/2023-18660.pdf

2 Fairness opinion and summary note

3 Please refer to the table below for the specific activities under the preferential treatment rule

4 Please refer to the table below for the specific activities under the preferential treatment rule

5 Please refer to the table below for the specific activities under the restricted activities rule

6 Please refer to the table below for the specific activities under the restricted activities rule

7 Rule 211(h)(2)-1

8 Clause 11, SEBI (Alternative Dispute Resolution Mechanism) (Amendment) Regulations, 2023

9 Regulation 22 (c), AIF Regulations

10 Master Circular for AIFs, SEBI circular SEBI/HO/AFD/PoD1/P/CIR/2023/130, July 31, 2023 (“AIF Master Circular”)

11 Consultation paper on proposal with respect to pro-rata and pari-passu rights of investors of AIFs, May 23, 2023

12 Regulation 15 (1)(b), AIF Regulations

13 Regulation 3(4)(b), AIF Regulations & Regulation 16(1)(c), AIF Regulations

14 Regulation 22 (g)(iii), AIF Regulations

15 Regulation 3(4)(c), AIF Regulations

16 Rule 211(h)(2)-3

17 Rule 206(4)-10

18 180 days in case of a fund of funds.

19 Regulation 22(g) and regulation 22(j), AIF Regulations

20 Rule 211(h)(1)-2

21 Regulation 22(b), AIF Regulations

22 Regulation 22(a), AIF Regulations

23 Quarterly reporting format, available at: https://www.ivca.in/regulatory-reports-sebi-circular

24 Rule 211(h)(2)-2

25 Regulation 29A, AIF Regulations

26 Modalities for launching Liquidation Scheme and for distributing the investments of AIFs in-specie, SEBI circular SEBI/HO/AFD/PoD-I/P/CIR/2023/098 dated June 21, 2023

27 Rule 204-2

28 Stewardship code, AIF Master Circular

29 Regulation 27 (1)(e), AIF Regulations

30 Regulation 27 (1)(d), AIF Regulations

31 Regulation 27 (1)(a), AIF Regulations

32 Regulation 30 and regulation 32, AIF Regulations

33 Rule 206(4)-7(b)

34 Clause 2.4, AIF Master Circular

35 Provided that it obtains a majority consent of investors and provides all investors with a note capturing the material terms of the credit line

36 Private funds prepare to spend billions on compliance after SEC rule, Financial Times

https://www.ft.com/content/6d39f967-e141-418c-aef0-76bb337c64ba

Disclaimer

The contents of this hotline should not be construed as legal opinion. View detailed disclaimer.

Research PapersHandbook on New Labour Codes Compendium of Research Papers Third-Party Funding for Dispute Resolution in India |

Research Articles |

AudioThird-Party Funding: India & the World The Midnight Clause |

NDA ConnectConnect with us at events, |

NDA Hotline |

VideoQ&A 2024 Protocol to the Mauritius India Tax Treaty Cyber Incident Response Management |